Ant Financial

History of how the “Ant” has become a giant

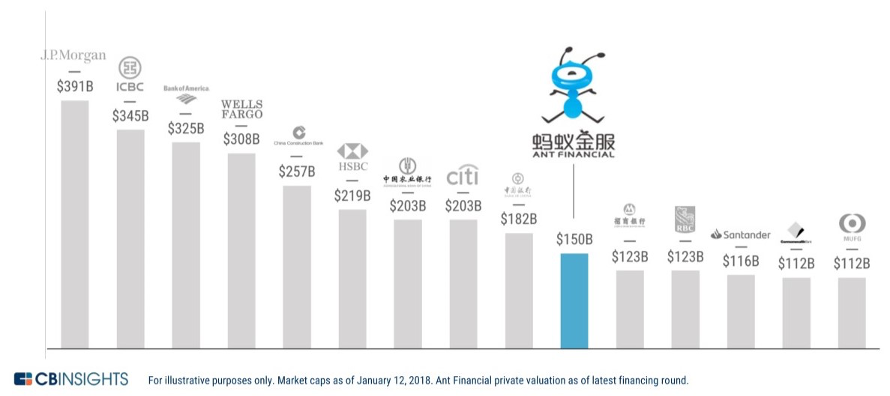

Ant Financial has raised 10 billion in 2018 at a $150 billion post money valuation, entering the top 10 of the most valuable financial services firms in the world. It is now more than ever worth it to discover what exactly this fintech giant is and how it was possible to scale in such a vertiginous way.

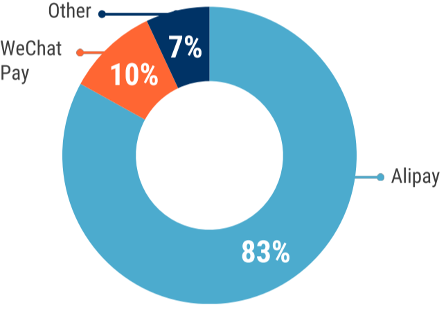

Nowadays the firm from Hangzhou offers a very comprehensive ecosystem of financial services that range from micro-credit to money transfers, passing through wealth management, insurance, and of course a digital payment system, that was the starting point of the ancestor of Ant Financial, Alipay. A lot more services are added year on year for both consumers and businesses.

This article will be a journey along the development of Ant Financial. It has not the claim to be exhaustive, but I’m sure that reading the next lines you’ll have the desire to know more of this company that is shaping China, fostering its growth, and going global.

History of Ant Financial (ex-Alipay)

In order to understand why in China mobile payments and Alipay developed so much we should look at the social and economic background of the country: the penetration of credit cards was very low, the Chinese banking system has always been controlled by the government and the banks lacked strong tech expertise. Last but not least, China was a rising market transitioning to a consumption-driven economics. Alipay has been able to offer solutions to the problems that this backdrop posed and to foster the development of a new market: the e-commerce.

Ant financial represents an evolution of Alipay, that was launched in 2003 by the e-commerce giant Alibaba just as a payment tool to support Taobao.com, its online shopping platform that was rising, but facing a tough competition in the conquest of the Chinese market. Alibaba invented Alipay to enable guaranteed transactions and thus increase the safety of online purchases.

In December 2004 Alipay was spun off from Taobao.com and became and independent payment system. In this phase it started to provide its payment services also to other retailers outside the Alibaba Group.

From 2004 to 2008 the focus of this new financial services provider was the internal market, where they exploited the first mover advantage in digital payments and the traction of Alibaba to get almost 50% of the total online transactions (47,6% in 2007). The chairman of Alibaba, Jack Ma, during the World Economic Forum of 2015 commented that thanks to Alipay the “Chinese e-commerce industry entered an era of safe payments”.

In 2008 Alipay formed partnerships with numerous foreign merchants and expanded outside China (Japan, Singapore, US…). Furthermore, they started to provide additional financial services, giving the sellers the possibility to borrow money up to 100,000 CNY (15.000 $) to finance their working capital. The same year they began to offer one-stop payment services for utility companies to allow their customers to pay the due bills. It was clear then how Alipay wanted to expand its financial services portfolio to revolutionize the life of the Chinese population in different areas and make their personal finance management easier.

From 2008, along with the increasing diffusion of smartphones, the target of mobile internet users in China expanded very rapidly, and this played an important role in the penetration of Alipay in the pockets of Chinese people.

In 2009 Alipay reinforced the presence in the travel booking industry working with 3 of the most important travel agencies (Ctrip, Elong and Mango) and continued to expand the scope of its financial services entering the insurance sector. The strategy in this market was to aggregate the offerings by the numerous insurance companies allowing the users to compare them and choose the most suitable for their needs. At this point in time the users of Alipay exceeded 200 million, with a growth rate of 100% on the previous year.

In the 2010s Taobao became the undiscussed leader of the Chinese e-commerce with its 80% of market share and Alipay followed the same glorious path, because most of the transaction on the platform were settled with it. In 2010 Alipay started effectively to be a fintech company, in fact partnering with UnionPay they released a pioneering payment service called “Instant Pay”, which allowed credit card holders to make online payments without opening online banking accounts. In order to do this Alipay acquired a third-party online payment licence from the People’s Bank of China.

In 2011 the payment services of Alipay were expanded from online to offline through the launch of “Barcode Pay”. This was a great evolution because it permitted Alipay to target also the traditional retail market together with the e-commerce. The comprehensiveness of the financial services offered plays certainly a major role in the lock-in of customers, that more and more can rely on the same service provider for different situations.

In May 2012, Alipay obtained a special payment licence for serving investment fund companies, that could then accept payments with Alipay. People became so able to invest their money as easily as never happened before.

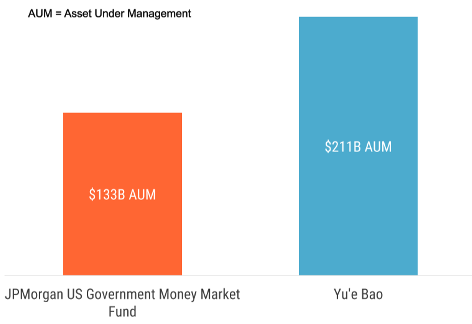

In June 2013, they entered directly the asset management market releasing Yu’E Bao, a mobile wealth management platform that was very flexible for the customers and granted also a 5% annualized return in 2013 thanks to the investments in money-market funds by Tianhong Asset Management Company, in which Alibaba Group was a shareholder.

In September 2014 Alipay obtained a licence from the China Banking Regulatory Commission (CBRC) to start its online banking business, MyBank, a bank with no brick-and-mortar presence. It’s exactly in 2014 that Ant Financialwas established to replace Alipay, which became just one of the segments of the new fintech giant.

In 2015 Ant Financial launched Sesame Credit, an innovative big data credit rating system based mainly on the transactions and payments history in Alipay, but not only. In fact, also the credit rating of the business partners is considered or the social networks of the applicant. The score ranges from 350 to 950, and depending on this it’s allowed to the customers to access different lending services and amounts.

Nowadays it’s under scrutiny the possibility by the government to use it as basis for the forthcoming social credit system, a utopian scoring system for the Chinese population. This possibility is raising a lot of concerns about the ethics of such a system, that would attach to everyone a number representing the quality of their behaviours as citizens, and would give the power to the government to reward and punish accordingly.

In 2018 Ant Financial brings to the market its blockchain platform with the main purpose of enabling the access to this technology to small and medium businesses, usually excluded from so advanced systems because of the prohibitive cost.

Ant Financial is now pushing on the development of local partnership with fintech players that use similar technologies in order to permit Chinese people to use their phones to pay and access financial services also abroad, and vice versa. At the same time, it is investing big amounts of money in acquiring or participating local partners, enabling them to build ecosystems driven by high frequency payments. There’s also a shift by Ant Financial from finance toward tech services, that are expected to generate 65% of its revenues in 3 years, compared to the 34% of 2017. In fact, Ant Financial receives royalties by the businesses that decide to use its services. The payment system is becoming day per day more a hook to enter the ecosystem of Ant Financial, rather than a final destination.

The ability of Ant Financial to foresee trends and lead the change is evident, exactly for this reason it will be fascinating to follow its next moves.

For those Fintech enthusiasts that are still curious about Ant Financial, the following parts will give information about the M&A carried out and the funding rounds that led to an evaluation of more than $150 billion.

Merges & Acquisitions

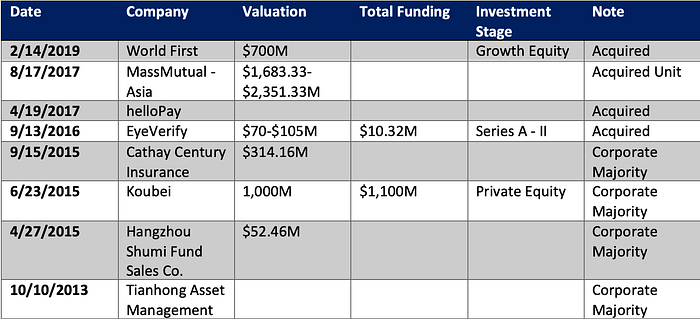

Since its establishment in 2013 Ant Financial has acquired 8 companies and made 110 investments in other firms, even without taking the control.

The reasons that led to the decision of acquiring those businesses are mainly strategic and in line with the long term objective of Ant Financials, summarized in providing inclusive financial services globally to underbanked consumer and small enterprises, granting at the same time security and top quality functioning.

Here we focus on the 3 main acquisitions by Ant Financial, that promise to help the growth of this already disruptive Chinese fintech unicorn.

Sep 13, 2016: EyeVerify ($70M)

EyeVerify is a security company that provides Eyeprint ID, a biometric verification solution for mobile devices. This patented authentication system uses existing cameras on smartphones to image and pattern match the blood vessels in the whites of the eye. Available on smartphones and tablets, the application protects data with a high entropy encryption key which is equivalent to a 50-character complex password. Requiring only a 1MP camera, this B2B solution enables businesses secure its customers. The company was founded in 2012 and is based in Kansas City, Missouri.

The lever of acquisition was certainly the implementation of the security system developed by the American startup in the financial services of Ant Financial. The relationship between the companies dates back to the year before the official acquisition, when they entered in a licensing agreement to apply the EyeVerify Eyeprint ID service into the Ant Financial’s payment authentication platform.

At the time of the deal, in 2016, the patented technology of EyeVerify was already trusted and used by more than three dozen banks and financial institutions. Thus, the solution had already been validated and raised the interest of a fintech giant like Ant Financials thanks to the easiness of introduction in the market, since there’s no additional hardware required, and the accuracy rate of 99,99%, deemed to be higher than that reached by fingerprint sensors.

Apr 19, 2017: helloPay

HelloPay is Southeast Asia’s latest payments solution. They are revolutionizing the way payments and money transfers are made, both online and offline. They provide a secure payment platform, created by an international team that is bringing together their extensive knowledge and experience in global payments to make sending and receiving money easier, both for personal and commercial use.

As a FinTech startup, they have investments from Tesco, J.P. Morgan, Verlinvest, Investment AB Kinnevik and Rocket Internet. They are present in Singapore, Philippines, Indonesia, Vietnam and are set to expand rapidly across South‐East Asia and Africa. HelloPay has a story that is somehow parallel to the one of Alipay, in fact it was founded in 2014 by Lazada, one of the e-commerce retailer leaders in southeast Asia, in order to develop the e-payment solution for its platform.

This acquisition by Ant Financial is completely logic and follows in the timeline a consistent investment of $1B made by Alibaba Group in the parent company Lazada. It is part of the ambitious expansion of Ant Financial outside the boundaries of China. HelloPay has been rebranded as Alipay Singapore, Alipay Malaysia, Alipay Indonesia and Alipay Philippines in the respective countries. Ant financial is following the strategy to make alliances, joint ventures or acquisitions to penetrate quicker the foreign markets, pushing on its economic strength. The size of this deal was keen private, and there are no data about it.

Feb 14, 2019: WorldFirst — $700M

WorldFirst facilitates businesses and individuals to conduct customer service and money transfer activities. Catering to clientele in the hedge fund and exporting sectors, the company helps businesses open up receiving accounts to get payments in their local currency and set up forward contracts to lock in a rate to make late transfers. The company also enables online sellers to manage their payments across multiple international marketplaces and make payments to overseas suppliers.

One of a number of globally active money remittance services, 16-year-old WorldFirst lets businesses and consumers move money between countries at prices that are lower than regular banks. This acquisition by Ant Financial is the first real move into the European market. Alipay and WorldFirst’s capabilities appear to be very complementary and the vision entails the expansion of the acceptance of Alipay in Europe, together with the addition of the international online payments and virtual account products of the British fintech company in the Ant Financial’s range of technology solutions.

This move can be seen also as a challenge to Amazon, that started to offer its own currency converter for non-American sellers, that operate on its e-commerce platform from foreign countries like China.

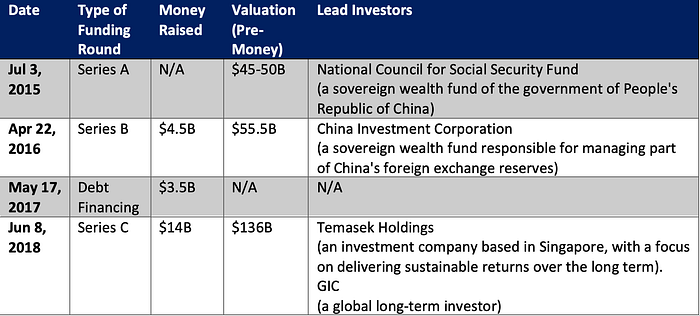

Funding rounds and valuation

The funding history of Ant Financial has led the company to become one of the most evaluated and capitalized of the world. We can clearly distinguish the 3 equity rounds that permitted to finance the expansion of this fintech company.

The A series in 2015 has not been like the usual ones, because indeed Ant Financial was spun out Alibaba and had already a great credibility in the Chinese market. So, the lead investor in this first formal round was the China’s largest pension fund, NSSF, followed by other major Chinese insurance corporations for an incredible pre-money valuation of approximately $45/50B.

The series B funding round happened just one year after, and it became immediately the biggest funding event ever in a tech company, surpassing the previous record of $3B raised by the Chinese Uber rival, Didi Kuaidi.

It’s with the C round of $14B that Ant Financial has entered the top 10 of the most valuable financial firms. This financing series, led by Temasek Holdings, saw the participation of both domestic and international institutional investors, including some of the most relevant banks like JP Morgan, Citi, Deutsche Bank, Morgan Stanley that acted also as financial advisors for the deal.

The dream to build an open ecosystem investing in technology and innovation is now running even faster than before, and actually one of the major focus of Ant Financial is in developing blockchain, AI and IoT capabilities and implementing them into its platform.

It seems quite clear that Ant Financial will likely be one of the Fintech leaders in the next years.

Author:

Sources:

Ant Financial: How a bug took on the world. (2019). Retrieved from AsiaMoney: https://www.euromoney.com/article/b1h7mtyfd5d8lg/ant-financial-how-a-bug-took-on-the-world

CB Insights . (2018). Ant Financial: Unpacking the $150B fintech giant.

Huillet. (2018). Alipay’s Parent Company Secures 14bln for Blockchain Development. Retrieved from https://cointelegraph.com/news/alipay-s-parent-company-secures-14-bln-for-blockchain-development

Lu, L. (2018, January). How a Little Ant Challenges Giant Banks?

Penn. (2016). Ant Financial Acquires EyeVerify. Retrieved from Finovate: https://finovate.com/ant-financial-acquires-eyeverify/

Russel. (2015). Alibaba Affiliate Ant Financial Confirms Series A Funding At $45-$50B Valuation. Retrieved from TechCrunch: https://techcrunch.com/2015/07/03/ant-financial-series-a/

Russel. (2016). Ant Financial, the Alibaba affiliate that operates Alipay, raises $4.5B at a $60B valuation. Retrieved from Techcrunch: https://techcrunch.com/2016/04/25/ant-financial-the-alibaba-affiliate-that-operates-alipay-raises-4-5b-at-a-60b-valuation/

Russel. (2017). Alibaba’s Ant Financial takes control of HelloPay to extend its reach in Southeast Asia. Retrieved from TechCrunch: https://techcrunch.com/2017/04/19/ant-financial-hellopay/

Russel, L. L. (2019). Alibaba’s Ant Financial buys UK currency exchange giant WorldFirst reportedly for around $700M. Retrieved from techcrunch: https://techcrunch.com/2019/02/14/alibabas-ant-financial-buys-worldfirst/

St Louis Business Journal. (2016). Alibaba subsidiary buys Kansas City startup, reportedly for $70 million. Retrieved from St Louis Business Journal: https://www.bizjournals.com/stlouis/blog/biznext/2016/09/alibaba-subsidiary-buys-kc-startup-reportedly-for.html?ana=RSS%26s%3Darticle_search&utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+bizj_stlouis+%28St.+Louis+Business+Journal%29

Stimolo, S. (2019). Ant Financial di Alibaba lancia fase test per la sua blockchain. Retrieved from The Cryptonomist: https://cryptonomist.ch/2019/11/12/ant-financial-alibaba-test-blockchain/

Wu, J. (2019). A Brief History of Jack Ma’s Ant Financial — the $150B Unicorn. Retrieved from Hackernoon: https://hackernoon.com/the-story-of-ant-financial-4t2aq3zh8